Money and the Military

A survey given to active and retired military as well as military family members found that 65 percent of members are stressed about finances, with 17 percent unable to focus on their military duty because of financial stress (prnewswire.com). Both the ordinary American citizen and military members face some of the same issues – debt and financial stress! Being a military member myself, I know some of the struggles that they go through, and I would like to explain some of those and ways to combat them, specifically looking at understanding responsible borrowing and the Blended Retirement System (BRS).

Borrowing

Military members are likely to experience frequent moves, bills which need management while deployed, as well as other stressors that lead to spending as a coping mechanism. Because of these factors, it is not uncommon for military members to hold debt. As we continue this conversation, it is important to understand that it is not a sin to borrow money, but issues do arise when an individual does not pay back the debt they owe. Unfortunately, many military members find themselves in so much debt that it causes significant stress.

I would like to encourage my fellow military member to NOT let debt rule over you; make the personal choice to pay back what you owe and get ahead in life. While it might seem crazy, an individual can start getting their financial freedom back by proactively setting up a budget which allows them to pay back current debt as well as save for the future, and this is how to start.

- First, decide the ideal amounts of money to be used in the different categories including savings (retirement, emergency fund, car, etc.), giving, lifestyle expenses, taxes, and debt and confirm that the amounts equal the amount of income coming in. Note: While the military may cover some expenses, it is still good to map out everything so that you can visualize how it is playing out.

- Next use an app, Excel, pen and paper, etc., to track all expenses and income to make sure your spending habits are actually reflecting the budget you initially created. This will also allow you to see where you can alter habits to spend less in one area in order to shift money into another area. For example, you could spend less eating out or move to an apartment with cheaper rent in order to pay more on a debt or save more.

- Finally, get an accountability partner that can review your spending routinely to make sure you are following the plan you set up for yourself and your family.

- And once you have a budget set up, you only need to make minor edits from month to month, year to year, as well as during a move or deployment.

On a personal note, during my freshman year of college I had no clue how to make a budget. As long as there was money in my checking account, I was spending it eating out, going out with friends, and on electronics purchases. Fortunately, through NEXUS, I was walked through how to make a budget on excel and began tracking my expenses. After a month, I realized I was spending $60/month on eating out! Keeping a budget helps a person see the little things that add up to a whole lot of money going out the door. I decreased my $60/month to $20/month and have $40 more to save.

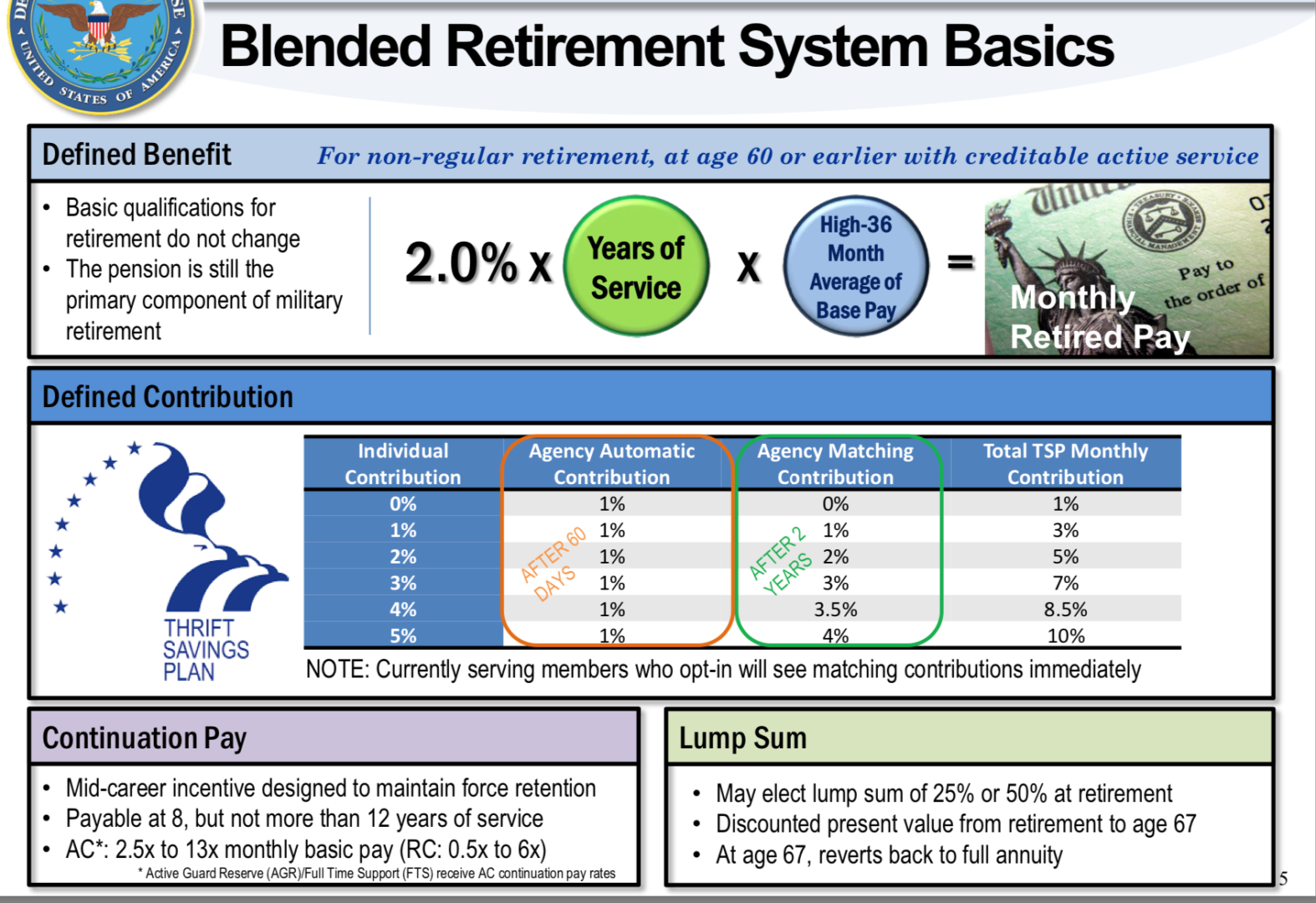

Blended Retirement System

Another area for which I have experienced military members having questions is with the Blended Retirement System (BRS). This “blends” a pension and a Thrift Savings Plan (TSP). The following diagram shows the benefits associated with the Blended Retirement System. Some important things to note in this diagram is that all service men and women are fully vested in the automatic 1 percent contributions, after finishing 2 years of service. This means that service members have rights to the full amount of the benefit. It works similar to a 401k in that the DOD will match what you put in. So, if you put in 5 percent of your base pay, the government will match that at 5 percent, and you will save 10 percent each year.

With the BRS taking the place of the legacy retirement system, it is important to note common misunderstandings with the system. First, service members need to be made aware of the 20 years of service difference. With the legacy plan, members have to serve a full 20 years to get 50 percent of their base pay as a pension each month after retirement. Not having 20 years of service means no pension with the legacy plan. On the other hand, the BRS gives you 40 percent of your base pay each month after retirement. A service member contributes up to 5 percent of their base pay to the plan, the government will match it dollar for dollar. When retirement comes in the BRS, a soldier can immediately take the pension; however, you need to wait until age 59 ½ to get the TSP out without a huge IRS penalty (MilitaryOneSource). Second, most service members do not understand why the military retirement system changed from the legacy to BRS. Under the traditional legacy system, those who served 20 years received a retirement benefit. As explained to me in my unit, that means around 81 percent of service members leave with no benefit at all. In the BRS, that is not the situation. According to militarypay.defense.gov, “85 percent of service members will receive a government benefit if they serve at least two years, even if they don’t qualify for a full retirement” (Militarypay).

If you would like help in coming up with a plan and/or strategies on finances and the military, set up a meeting with me through the following link: https://ronblueinstitute.com/schedule-an-appointment/.

References

BRS. (2018, March 28). Blended Retirement System Basics [Digital image]. Retrieved March 23, 2021, from https://militarypay.defense.gov/Portals/3/Documents/BlendedRetirementDocuments/BRS%20Frequently%20Asked%20Questions%2003282018.pdf?ver=2018-03-28-235150-797

Military One Source. (n.d.). Personal finance & financial security. Retrieved March 23, 2021, from https://www.militaryonesource.mil/financial-legal/personal-finance/

Z. (2018, June 29). Survey reveals 65% of military personnel are stressed about finances. Retrieved March 23, 2021, from https://www.prnewswire.com/news-releases/survey-reveals-65-of-military-personnel-are-stressed-about-finances-300273747.html